On March 12, Frontier Communications (FTR) rolled over secured 2021 debt of about $1.65 billion to 2027 and their revolver due in 2022 of $835 million to 2024. The $1.65 billion amount means they have cleared the runway to handle the Big Kahuna $2.2 billion debt due on Sept. 15, 2022. Moving the revolver to 2024 means it will be available if needed to help with the 2022 payment plan.

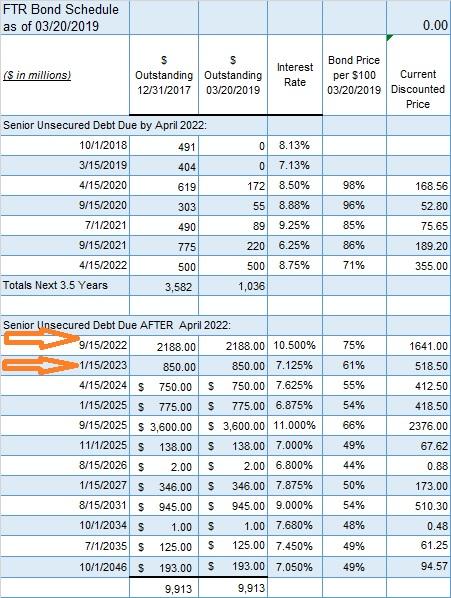

If we look at the latest Bond Schedule list, we can see that things have changed considerably just since Fiscal Year 2017.

1. Notice that in the 03/20/2019 column amounts are much lower than they were just 15 months ago. The total due prior to 2022 is down $2.5 billion from $3,582 to $1,036 billion. Most of the decrease was a rollover of debt to later years but FTR has also paid off two bond issues worth about $800 million in the last 5 months. The numbers are from the 2017 and 2018 10-Ks. That is excellent debt management in my opinion.

2. Next look at the two arrows. Those point out the looming problem of over $3 billion due in a 4-month period from 09/15/2022 to 01/15/2023. But that is 3 years and 6 months from now.

3. Then look at the bond price in the last column showing the two arrow bonds selling for 75 and 61 cents on the dollar, a substantial discount in anybody's book.

So what does FTR do about this looming debt crisis? They use their ever-increasing free cash flow to buy the arrow-marked debt back at a discount. That's because the list price of those 2 bonds is $3,038 billion but the discounted price is $2,160 billion, a savings of $878 million.

How much FCF will FTR have over the next 3.5 years? I am going to say $2.8 billion or an average of $800 million per year. The current estimated FCF for 2019 is $625 million but that is low I think because of interest savings on paid off debt (about $20 million), increased FCF coming from the $500 million EBITDA effort, increased revenue (finally) and if need be lower CAPEX. For example, interest savings will increase if they buy back the 09/15/2022 debt at 75%. In that case, they are earning 14% interest (2188/1641 * 10.5%= 14%) on invested buybacks.

In fact, at the current discount, all bonds due by 2024 could be bought back for $2.667 billion which is less than my $2.8 billion FCF estimate.

Of course, it is not going to happen exactly like that but the point is FTR has the FCF needed to make a substantial dent in the 2022-2023 bonds.

So how much would they need to pay off to allow them to roll over whatever is left? Per the 2018 10-K page F-25 (see here), the outstanding long-term debt as of 12/31/2018 stood at $17.4 billion. Then in March FTR paid off $404 million lowering the number to $17 billion. We know for certain that FTR can easily pay off all the $1.036 billion in debt due before Sept. 2022 so that would leave $16 billion due.

Now let's be conservative and say FTR could pay down another $1 billion of their debt from their $2.8 billion FCF and with the discounted bond price actually retire $1.2 billion.

That gets us down to $14.8 billion as of Mid-year 2022.

The $500 million EBITDA improvement plan runs to the end of 2020 but in actuality, FTR has another 18 months (until mid-year 2022) to get to the $500 million before the rollover is needed. Current EBITDA is about $3.6 billion so by 2022 it should be at least $4.1 billion.

That puts the Debt/EBITDA ratio at mid-year 2022 at a relatively (for FTR anyway) minuscule 3.6x (14.8/4.1). And this using only about 72% of the FCF estimate for the time period between now and mid-2022. That 3.6 ratio compares to Sprint's (S) 3.3 and AT&T (T) 3.0. The indebtedness limit in the indentures is 4.5 so FTR will be way below that.

From the 2017 10-K:

" Among other things, these covenants limit our ability to incur additional indebtedness if our leverage ratio exceeds 4.5 to 1"

And remember they are not going to be adding to indebtedness just rolling over current indebtedness. So the 3.6 Debt/EBITDA ratio will not change.

And CEO McCarthy agrees:

"We believe that executing on our priorities will over time expand the range of options for leverage reduction, including the ability to refinance our longer-dated unsecured maturities in the high-yield market."

As I have said before if bond buyers loaned FTR money at 4.5x, why wouldn't they do the same at 3.6x? A legitimate question though would be at what interest rate? With the Federal Reserve basically freezing rates for 2019 and former Federal Reserve Chairman Janet Yellen calling for interest rate cuts, this may not be the problem that it seemed to be last year.

It's apparent from the following charts that the bond market likes what's happening. The value of the 2022 and 2023 bonds went up after the 4th quarter presentation on Feb. 22 and then again when the rollover happened on March 13.

Chart source: FINRA

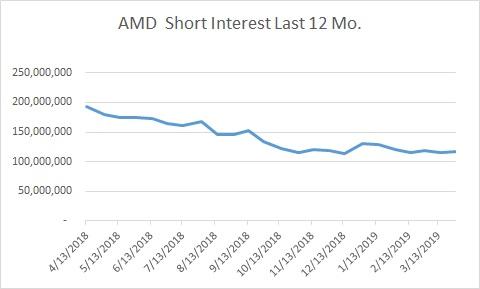

Many writers emphasize how highly shorted stocks should be avoided and that is often true. However, by their very nature turnaround stocks usually have a higher short interest ratio than other stocks. If they didn't their price would be much higher and their turnaround potential much lower. So if you specialize in 'Turnaround Stocks' as I do, shorts can be your friends.

FTR short interest has steadily climbed over the last 12 months as financial results, although improved, have still lagged expectations.

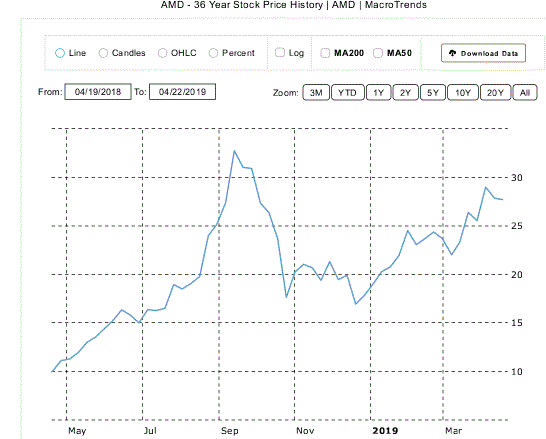

Short sellers are of course not always right which is why fundamental analysis is so important when facing off against short sellers. I explained how this worked with Advanced Micro Devices (AMD) "AMD: 5 Reasons The Shorts Will Be Changing Their Shorts Shortly."

Notice how AMD's short volume has decreased while the stock price has more than doubled since I wrote that article. In a surviving FTR's case, a modest 3 times FCF (free cash flow) results in a $20+ price.

Source: Macrotrends

Risks:Of course, FTR is not without substantial risks. If revenue continues to decrease substantially over the next two years, achieving the new EBITDA goals will be difficult or impossible to reach. Also if they roll over debt in the future, interest rates may be substantially higher and affect the entire plan.

And finally, they compete in a market that has much larger and more financially stable competitors and as such their plans may not succeed as described in this article.

This is certainly not a widows and orphans stock.

Conclusion:If in mid-2022, FTR's EBITDA, FCF and revenue are growing and their debt and interest charges are declining, why would they not be able to roll over their debt?

FTR will report first quarter results after hours on April 30. I expect to see a quarter-over-quarter revenue increase per this statement from McCarthy.

"I think the trends out of the fourth quarter remained very stable as we went into the first quarter, as we're in the second month of the first quarter we still remain very strong. So I feel very good about the first quarter, from a revenue perspective."

If revenue does increase, the shorts will begin to head for the exits and we should see the stock price jump considerably. I would say revenue increases are the single most important factor in moving FTR's price higher. If revenue goes up, other financial measures will improve also.

FTR remains a strong high-risk buy.

You can see all 10 of my FTR articles here.

If you found this article to be of value, please scroll up and click the "Follow" button next to my name.

Note: members of my "Turnaround Stock Advisory" service receive my articles prior to publication, plus real-time updates.

Disclosure: I am/we are long FTR. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.